Some payday loans have interest rates as high as 664% – but now Minnesota will cap them at 36%, in line with some other states.

Meka Armstrong of Detroit, Michigan, has struggled in a cycle of debt from payday loans for years. She first took out a payday loan in 2010 to cover the costs of medication she needs as she is disabled and lives with lupus.

“Worst decision I ever made,” said Armstrong. “The interest rate was 49% and I thought I would get my medications and pay the money back, but when I paid the money back, it left me with nothing. That’s how they get you. I, unfortunately, started the payday nightmare, and you can’t get out of the loop.”

Armstrong is just one of the 12 million Americans who take out payday loans annually in the states where payday lending is not prohibited, shelling out up to $9.8bn in fees to payday lenders every year. The industry targets Black borrowers such as Armstrong, and Latinos, who are more likely to have lower credit scores and be unbanked compared with their white counterparts.

A payday loan is a short-term, high-cost loan typically due on an individual’s next payday. But the payday industry thrives and depends on borrowers who take out numerous loans and face exorbitant fees and interest rates when they can’t keep up. Payday lenders collect 75% of their fees from borrowers who take out 10 or more loans a year, according to the Consumer Financial Protection Bureau.

The average payday loan customer has an annual income of about $30,000 and four in five payday loans are rolled over or renewed. The average payday borrower stays in debt for five months, paying $520 in fees to borrow $375 on average. The majority of borrowers, seven out of 10, take out payday loans to pay rent, utilities or other basic expenses.

It took Armstrong years to get out of the debt cycle, which she said was difficult because the payday lenders have borrowers’ bank account information, can sue them and even threaten them with jail time for nonpayment.

During the Covid pandemic, Armstrong had to take out another payday loan, even though she had previously experienced the debt trap and the consequences of doing so, because she caught Covid in 2020 and was sick.

“It’s embarrassing because I know how predatory they are, but I had Covid-19 for 98 days, almost died, my whole house was sick and we were behind on bills,” she added. “I’m still in the payday nightmare because of that desperation unfortunately.”

The debt trap is very much by design and it’s how payday lenders’ business model works

Yasmin Farahi of the Center for Responsible Lending

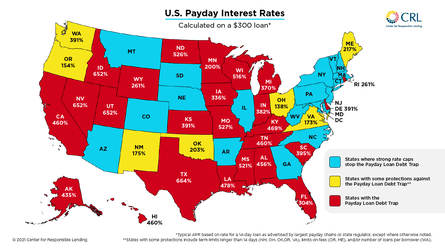

The US has a poor record when it comes to regulating payday lenders. Currently 20 states and Washington DC have enacted rate caps of 36% annually or less to rein in the cycle of debt that traps consumers who take on payday loans, aligning these states with the federal Military Lending Act passed during the George W Bush administration that capped annual interest rates on consumer loans for active duty military at 36%.

In states without caps, the average annual interest rate for payday loans is about 400% and as high as 664%.

“The debt trap is very much by design and it’s how payday lenders’ business model works,” said Yasmin Farahi, deputy director of state policy and senior policy counsel at the Center for Responsible Lending. “They succeed by making sure their customers fail. They target low-income communities and communities of color, and it’s a model that’s based on their customers failing, essentially, for them to stay in business and generate fees.”

In Minnesota, the state legislature recently passed a law to cap interest rates on payday loans to 36% annually, from average annual interest rates in the state of 220% in 2022.

Opponents to the legislation claimed the cap would deter lenders from doing business in Minnesota, though advocates have countered that this has not been the case in states where similar legislation has already been enacted.

“It’s meant to be a continuous cycle,” said a payday loan recipient in Minnesota who requested anonymity. “You end up having an emergency, and then you think that, OK, I can pay this off, it’ll be a one-time thing and that’ll be that, but then your next paycheck comes, and it comes out of your bank account automatically and then you’re essentially just back where you started. So then you have to take the same loan out, basically the same day that you pay it off. And it just keeps going and going and going every payday.”

Anne Leland Clark, the executive director of Exodus Lending in Minnesota, supported the cap. The legislation was split across partisan lines with Democrats introducing and supporting the bill though polling across political lines showed 79% of Minnesotans supporting a 36% or lower interest rate cap.

Prior to Democrats in Minnesota winning a trifecta majority in the state government in November 2022, efforts were made at the local level to enact interest rate caps.

No longer will people be turning and getting into debt traps, where their ability to repay is not accounted for

Anne Leland Clark of Exodus Lending

“No longer will people be turning and getting into debt traps, or balloon payments, where their ability to repay is not accounted for,” said Clark.

She noted a provision was added to the legislation that would permit lenders to charge 50% annual interest rates as long as they report doing so, but Clark noted her organization will be monitoring to see how lenders utilize the provision.

“When you crowd out the predators, people are going to turn to and find the more responsible lenders and the more responsible lenders are going to license in your state,” Clark added.

Jason Ward, a bankruptcy lawyer in South Carolina, where payday lending is permitted and unregulated, said over half of his clients filing for bankruptcy have at least one payday loan.

The average annual interest rate for a payday loan in South Carolina is 385 %.

“The interest numbers are so high that I honestly don’t believe the payday loan companies even intend to get paid back,” said Ward.

He said many of his clients take out the loans out of desperation to cover basic expenses and that desperation is taken advantage of by payday lenders who know many clients will accept loans with exorbitant terms because they are just focusing on trying to survive at the present.

“When you weigh how desperate somebody can be with what’s being offered, you get the sense that it can be predatory,” Ward said. “I don’t think people understand the desperation of a lot of people’s situations.”